This is the most difficult post I have ever written; the story is complicated and sorely disappoints me. I realized that I could no longer work with the Village of Hartland Board and resigned my appointment to the Village’s new Environmental Corridor and Open Spaces Task Force, even though it was mostly because of my efforts that this task force was created.

When Wendi M. Unger, CPA, Partner, Baker Tilly presented the 2015 Village of Hartland Audited Financial Statements to the Board on May 23, 2016, I was all ears. That may sound like a pretty dry topic to get excited about, but I’ve been frustrated and dismayed by the reluctance on the part of the Village of Hartland leadership to apply the resources necessary to take care of all of their land, especially given the strong financial position of the Village. The Village Department of Public Works (DPW) has, without the Board’s explicit approval, implemented a policy over the years of partitioning Village Land into maintained and unmaintained areas: If it’s mowed around, it’s maintained, if not, forget about it. Obviously, this keeps costs down, but over the years the unmaintained areas of Village properties like Penbrook Park have become seriously degraded and overrun by invasive species like buckthorn and garlic mustard.

During her presentation, when discussing the $321,463 excess in actual expenditures for TIF (Tax Incremental Financing) over the estimated expenses (see page 45 in the 2015 Audited Financial Statements), Ms. Unger mentioned in passing land that was donated to the developer. That got my attention and I began to investigate to find out — Who was the lucky developer?

I checked the Village of Hartland 2015 Audited Financial Statements and found no footnotes explaining the TIF expenses. Ryan Bailey, the Village Accountant, explained that this is kosher per the Government Accounting Standards Board, but it’s definitely not transparent. You will see below that, per GASB standards, a municipality can make taxpayer funded gifts to developers without revealing them in their financial statements. It is possible that my questions to Ryan about the TIF expenses may have prompted his letter to the Village Board dated June 20, 2016 where he wrote:

The State of Wisconsin mandates that all TIF District’s have audits when each of the following occurs 30% of project plan expenditures is met, 100% of project plan expenditures is met, and the close-out of the TIF District (maximum of 23 years after the creation). TIF #4 has reached the 30% and 100% of project plan expenditures as stated in the TIF plan document and requires an audit. Staff has requested an engagement letter from Baker Tilly for the TIF audit. Baker Tilly anticipates the fee to be approximately $2,500-$3,500 for the audit and audit report that will be prepared.

The close-out TIF audit will happen when the TIF has created enough increment to offset expenditures and eliminate the TIF’s negative fund balance. Currently TIF #4 has a fund balance deficit of $649,220. TIF #4 was shrunk down to two parcels last year in the hopes of gaining some positive increment to help offset as much of the fund balance deficit as possible. Depending on the increase of property values this TIF will take a while to overcome this deficit and eventually close out.

This is a full year after the triggering events — but better late than never. I’ll be interested to see the results of that audit, and you might be too, after you read the story below. God forbid they should resurrect the Joint Review Board to review the audit. But I’m getting ahead of myself.

In 2009 the Village of Hartland purchased two properties, HAV 0424032 and HAV 0424033 for a total of $415,487. At a time of depressed real estate values, the Village paid a premium of almost $62,000 above the $353,100 assessed value for the two properties. The buildings were razed and the land was conveyed/given/ceded/transferred/donated, at no cost, to JD McCormick, LLC as part of the Village’s incentive package to develop the Hartland Riverwalk Apartments. This project was packaged as TIF District 6 and described in the Lake Country Reporter.

The LCR story includes : “Cox said that McCormick initially requested more than $1.93 million in financial support and the no-cost transfer of two village-owned parcels of land to assist in the redevelopment of the Riverwalk site, between East Capitol Drive and Lawn Street. He later agreed to the reduced figure.” Yes, he did agree to a reduced figure of $1.75 million, but the story fails to confirm the fact that the, “no-cost transfer of two village-owned parcels of land”, was included in the deal, nor does it mention the cost to the Village of these two parcels.

Joint Review Board

The Village of Hartland had decided that TIF District 4 was not working out as they had planned and, in its current configuration, it could not support the new apartment development they had in mind. So they proposed an Amendment to TIF District 4 to remove all but two parcels, and the creation of TIF District 6 to support the Riverwalk Apartments development project. The Village was obligated by Wisconsin Statutes to create a temporary Joint Review Board and submit their TIF District proposals to them for final approval. The JRB consists of representatives from the overlying taxing authorities including: David Lamerand, President of the Village of Hartland Board; Norman Cummings, head of the Waukesha County Department of Administration; Cary Tessmann, Vice President – Finance Waukesha Area Technical College District; Diana Taylor, Hartland-Lakeside J3 School District; Steve Kopecky, UHS District of Arrowhead Union High; and Connie Casper, Public Member. They are interested parties because a portion of the tax revenue they get from the Village is diverted to cover the expenses of the TIF Districts.

At a Joint Review Board meeting on 3/12/15 Norman Cummings asked Village Administrator Dave Cox directly if the Village had paid more than the accessed value for the two properties mentioned above:

Mr. Cummings: So I assume you paid more than the assessment today on those two parcels

Administrator Cox: We paid less than they were assessed

Dave Cox was not the Administrator of the Village at the time these properties were purchased and perhaps he was simply confused or mistaken. Ryan Bailey, the Village Finance Director/Treasurer, and Village Board President, David Lamerand, were at the meeting and chose not to correct Administrator Cox — maybe they forgot how much the Village paid. You can listen to the 3/12/15 JRB meeting here, the relevant discussion begins at 3:00.

On May 27, 2015 the JRB met and had a substantive discussion despite the fact that the first chance they had to review the documents for the complex and detailed proposals was at the time of the meeting. The Project Plans for the TIF District 4 amendment and the creation of TIF District 6 that they reviewed are linked here and you can listen to the audio of the meeting here (note that the recording I got from the Village Clerk does not start at the beginning of the meeting). Village Administrator Dave Cox, Village Attorney William E. Taibl and James Mann from Ehlers (a municipal financial advisory company) were also present. There are a couple of noteworthy exchanges that I want to point out, the first is concerning TIF District 4:

Mr. Cummings: How much more is being added to the $500,000 that has been spent so far?

Mr. Mann: Its not anticipated that there’s going to be any additional expenditures in TID 4.

Mr. Mann and Administrator Cox repeatedly make the claim that no further expenses will be charged to TIF District 4 in 2015 when they should be aware that $143,000 of additional expense will be charged to the district when the Village conveys the two parcels of land they own to McCormick as part of the TIF District 6 deal (the shell game).

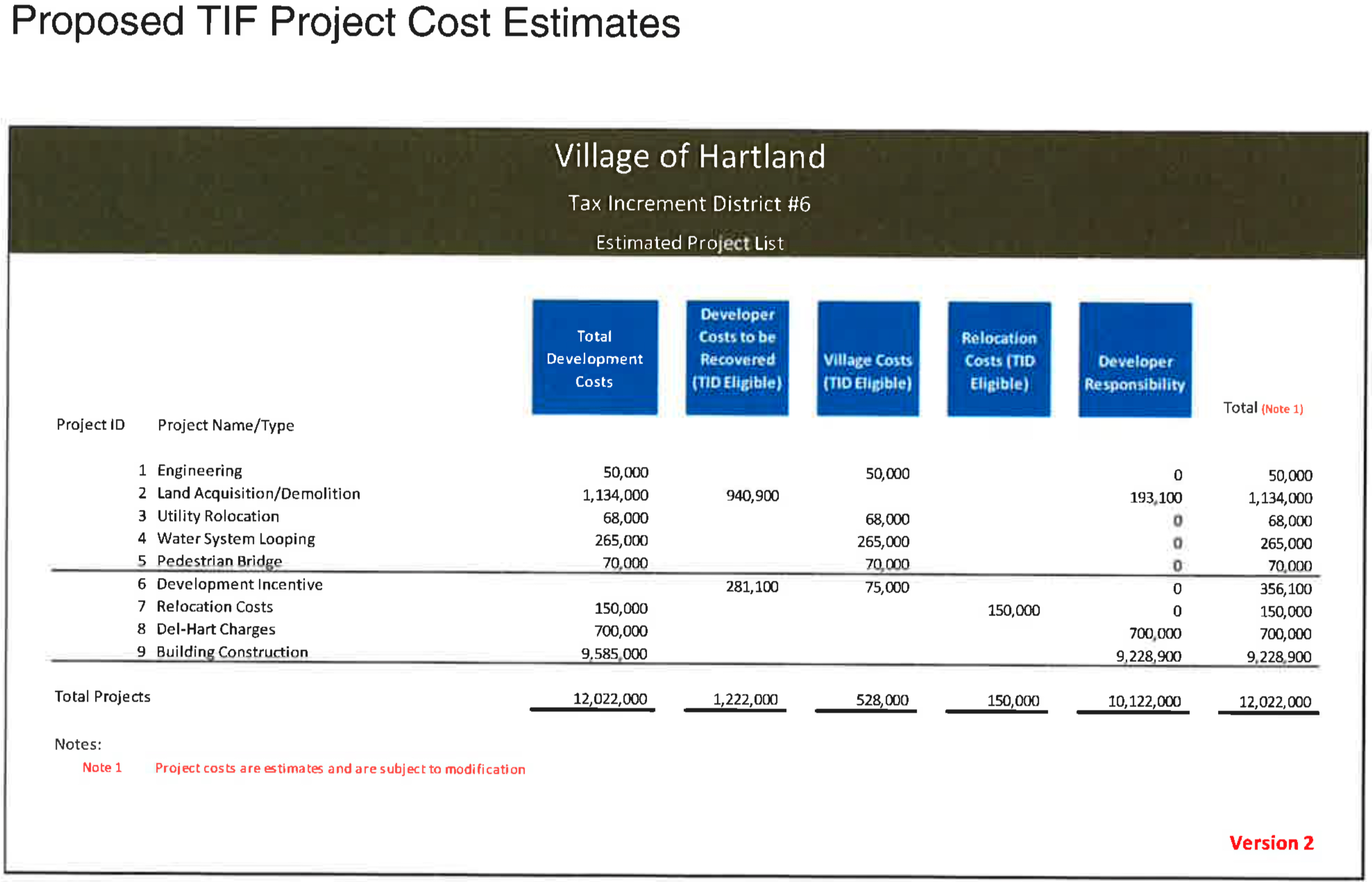

The other conversation I want to highlight here concerns the creation of TIF District 6. Below is Version 2 of the Project Costs table from page 16 of the Project Plan that they are referring to in the discussion. But please note that they were looking at Version 1 of the table, which is not available, so Version 2 below reflects the Village’s attempt to implement the changes recommended by Mr. Cummings.

Mr. Cummings: How much is the developer paying besides the cost of construction? I mean is this TIF picking up everything?

Mr. Mann: No

Mr. Cummings: It would be real helpful to know what the developer’s contributing versus the taxpayers.

Mr. Mann: The developer is contributing 2 million dollars of sunk cost, umm, for the purchase of the land.

Mr. Cummings: And what’s the land assessed at? What’s the equalized value of the land?

Mr. Mann: The equalized value of the land as it stands right now is 1.3 million dollars.

Mr. Cummings: Then why is he paying 2 million?

Mann: Some of that has already had structures removed.

Mr. Cummings: Yeah Ohh.

Mr. Mann: So the value of the land has already had structures removed. Those structures were removed before.

Mr. Cummings: And so, would this, would this have sold for 2 million if it’s not for TIF? I mean are we basically, you know, I’ve seen other projects here where we’re basically paying more than what it’s worth by using tax dollars. It shouldn’t work that way.

Mr. Mann: I mean you’ve got a million dollars just in the land value of the two remaining structures that are on the property.

Mr. Cummings: The structures are going to be removed right?

Mr. Mann: Correct.

Mr. Cummings: So there’s no value to anybody.

Mr. Mann: Correct and that’s the problem we have to spend a million dollars to start this project.

Mr. Cummings: Ok, I understand from the developer’s standpoint, but why are we paying the property owner so much money when it’s not going to sell? Why are you paying him $700,000 more than it’s equalized value?

Administrator Cox: Jim what are you including in the 2 million acquisition costs?

Mr Mann: Well you’ve got, I mean I’m just looking at our project list in terms of what we’ve got included in the project plan itself.

Mr. Cummings: I’m talking about the developer’s costs, you said he paid 2 million for the land.

Mr. Mann: He is 2 million of cost which he’s included.

Administrator Cox: It’s not just the land.

Mr. Mann: His equity into the project.

Administrator Cox: He has, and maybe Norm, maybe you asked something we didn’t answer to it. He’s acquiring the strip mall itself for, call it a million dollars, its a little less than a million dollars, he’s acquiring, he had acquired already, ahh, the residential property adjacent to the subdivision contributing…

Mr. Cummings interrupts: Did he remove the buildings?

Administrator Cox: No. And then the Village has the two parcels that it acquired and removed the buildings that he’s acquiring, ahh in this process. And so there’s some costs there and then I don’t know what else he’s got, demolition costs and probably utility work and those kinds of things, that are in there that the Village is supporting.

Mr. Mann: Site prep.

Mr. Cummings: How much is the Village being reimbursed for their, for their costs?

Administrator Cox: The Village has a carrying cost of $143,000 on the properties (note, he fails to disclose that the Village paid $415,487 for the two properties in 2009). Ah, the transaction will probably wash to the Village will get nothing for that, it will be part of the deal.

Mr. Cummings: Well it would be real helpful, and I just saw this in Sussex what they did, because they also had a area that was very difficult to develop. They had a column of developer costs, they had a column of what the Village has contributed, and they had a column of what the TIF is contributing. It goes a long way to showing us how much went into making this thing work.

Administrator Cox: OK.

Mr. Cummings: And showing us how much your contribution has been. I wouldn’t have known that if you just didn’t tell me that (note, it is not explicitly mentioned in any of the project plans or meeting agenda packet documents). And I’ll have more comfort voting for something where I see all the effort that’s been made both by developer and by the Village.

Administrator Cox: OK.

Mr. Cummings: So maybe I should get you a copy?

Mr. Mann: No, I understand.

Mr. Cummings: It’s a simple concept.

Mr. Mann: No, I Understand what you’re talking about very similar to what we did in the Delafield TID. And I don’t know the Sussex one but I understand.

Mr. Cummings: Yes and I remember the Delafield TID, you’re talking about the residential multi-family?

Mr. Mann: Yeah.

Mr. Cumminngs: That’d be very good.

Mr. Mann: OK.

Mr. Cummings: That would also go a long way, you know when we go back to our respective boards etc. it goes a long way to illustrating…(interuppted)

Ms. Tassermann: That its more of a partnership.

Mr. Cummings: Particularily if I’m hearing that, you know, the developers paying 2 million for you know 1.3 million assessed, but then there were also a lot of costs that are going in by the Village and the developer in preparing, already preparing the properties.

Mr. Mann: And there are some extraordinary costs in doing the development as its laid out. And that’s, you know, you’ve got, you’ve got costs for the underground parking, so I mean basically you’re paying for density.

Yes indeed, it would have gone a long way towards explaining the total costs that were going into the project at the upcoming Public Hearings on June 4, 2015 and June 22, 2015 if the Village had included the three columns: Developer Costs (not including TIF District eligible costs), Village Costs (not including TIF District eligible costs) and TIF District Costs, on the project costs table — as Mr. Cummings suggested — and listed the $415,487 it paid back in 2009 for the two parcels it gave McCormick as part of Village costs. But, apparently, Administrator Cox, President Lamerand and Jim Mann didn’t want to go the long way and the table (Version 2 shown above) was not updated per Mr. Cummings’ recommendation prior to distribution at the Public Hearings.

Joint Architecture and Plan Commission Meeting and Public Hearing June 4, 2015

What bothers me is that the $415,487 paid for the two properties was expensed to TIF District 4, and that gift was never mentioned as part of the incentives offered to McCormick to develop the Hartland Riverwalk Apartments during the Public Hearing for the Project Plan for TIF District 6 that was held by the Joint Architecture and Plan Commission at their June 4, 2015 meeting. Village Board President Dave Lamerand ran the meeting and Administrator Cox and Jim Mann made the presentation, which you can listen to here. There were two relevant resolutions on the agenda: Reduce the number of parcels in TIF District 4 and create TIF District 6.

Administrator Cox began:

Because TIF District 4 is in a negative increment, that is, since it was created in 2008 it has lost value, the proposal here in front of the Plan Commission at this moment is to reduce the size of TIF district 4.

Now, imagine you were one of the “public” present and you’re not an accountant and you haven’t read Wisconsin Statute 66.1105 recently and you’re scratching your head and thinking, ‘man, that sounds bad — it’s in a negative increment‘. Unfortunately, no one present asked what a “negative increment” was, or how they had reached that conclusion, and no explanation or documentation was offered. I tried to figure it out and found that it is not based on assessed values, rather, it is based on an arcane concept called equalized value. The Wisconsin Department of Revenue (DOR) calculates the equalized values for all the TIF Districts in the State and you can find the value increments for Hartland’s TIF District 4 in the links provided at the bottom of this DOR website.

| 2009 | (5,069,200) |

| 2010 | (13,896,200) |

| 2011 | (14,663,800) |

| 2012 | (4,996,900) |

| 2013 | (708,700) |

| 2014 | (389,600) |

| 2015 | 503,800 |

On page 1-17 of the WISCONSIN’S EQUALIZED VALUES document it says:

The Equalized Value is the estimated value of all taxable real and personal property in each taxation district, by class of property, as of January 1, and certified by DOR on August 15 of each year

We can see from the table above that TIF District 4 was trending towards a positive increment i.e., like real estate all over the country, it was slowly recovering value from the 2008 financial crisis, and had, in fact, attained a positive increment as of the January 1, 2015 DOR estimate. This precedes any amendment made to TIF District 4 by the Village in 2015. This information should have been documented and explained during any discussion about the “negative increment” at the Public Hearings, Village Board meetings and JRB meetings, but it was not. The notion that TIF District 4 was in a “negative position/increment” was a red herring. (Please note that I found out on July 29, 2016 that the preliminary values for the current year are not made available by DOR until August 1, giving municipalities a chance to review them before certification. The final numbers are certified on August 15 and then published on their website. So, technically speaking, TIF District 4 was in a negative increment at the time Administrator Cox made his presentations.)

So that’s the basics of the proposal that is under consideration tonight. There’s really no change in the project plan, with the one exception of modifying the expenses in the district, which is shown on … (Jim interjects “page 10”) .. on page 10 of the plan, we have some copies of the plan around if somebody wants to see them. But basically page 10 of the plan shows the project expenses as they were in the original project plan, ahh, the anticipated, the plan there, the the adjustment there will be to bring those down to the actual expenses of the district, which are right around $600,000 and show that that’s the end of the expenditures. As you see there is a little footnote underneath the table that says there aren’t any anticipated additional expenditures because we’re done with the district and we’re reducing its size to the only parcel that’s been redeveloped or going to be redeveloped. So that’s the basics. Jim, I don’t know if there anything more really to add.

They may have been “done with the district”, but they weren’t done expensing the two parcels mentioned above, which were still carried on the books as property for resale at $143,000. Ryan Bailey explained it to me in an email:

Both of these properties were purchased in 2009 for a total of $415,487 (the sum of $221,383.49 and $194,103.51)…then the houses on these properties were demolished leaving a total value of $143,200 (the sum of $78,800 and $64,400). So in 2009, TIF #4 recognized expense of $272,287 and held an asset of property for resale of $143,200. Then in 2015 when TIF #6 was created and the property was transferred over to the developer, the Village recognized the remaining $143,200 expense in TIF #4.

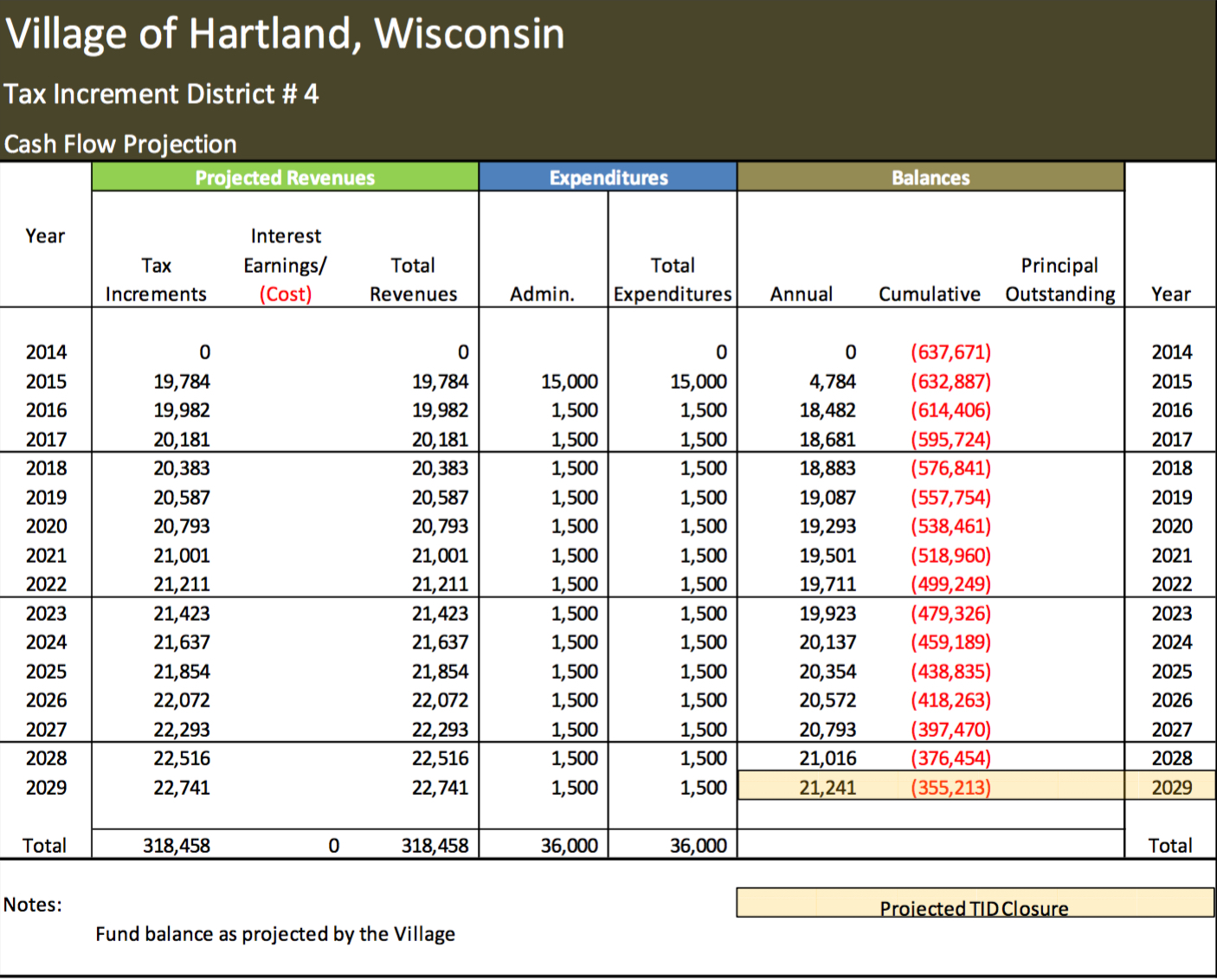

I think it dawned on Administrator Cox and Mr. Mann, or maybe someone whispered in their ears, that they were forgetting, or neglecting, to recognize the additional $143,000 of expense that was soon to be charged to TIF District 4. We can see this reflected in the update they made to the TIF District 4 Costs table on page 14 between the 5/26/15 and 6/22/15 versions of the table (The Buckthorn Man thinks the land deal with McCormick went down sometime between 5/27/15 and 6/22/15 and that is why the Cash Flow Projection table was updated).

Here is the 5/26/15 version of the table on page 14 of the TIF District 4 Project Plan, distributed at the June 4, 2015 Joint Architecture and Plan Commission Public Hearing, and note the beginning deficit balance of (494,471).

Then, prior to the Village Board meeting and Public Hearing scheduled for June 22, 2015, they updated the table and note the new beginning deficit balance of (637,671), which reflects the recognition of an additional $143,200 of expense — the carrying costs for the two parcels of Village land.

Then, prior to the Village Board meeting and Public Hearing scheduled for June 22, 2015, they updated the table and note the new beginning deficit balance of (637,671), which reflects the recognition of an additional $143,200 of expense — the carrying costs for the two parcels of Village land.

The transfer or conveyance, euphemisms for GIFT in this case, of the two Village owned parcels to McCormick was not explicitly referenced in any documents made available by the Village until it released the PLANNED UNIT DEVELOPMENT AND TAX INCREMENTAL DISTRICT AGREEMENT for TIF District 6 in the Meeting Agenda Packet for the June 22, 2015 Village Board Meeting. Unfortunately, the draft of this document dated June 10, 2015 was not distributed at the Public Hearing on June 4, 2015.

Dave handed off to Jim Mann and he elaborated:

You really said everything I was going to say. Basically the reduction would allow a greater amount of increment to be generated in the tax increment district. And, cashflow wise, at the end of tax increment district, it probably will not recoup all of the dollars that were expended, but you have a better chance of coming close to recouping those dollars by shrinking it and removing those properties that have lost value. So the true increment can flow back to the district to recoup those costs.

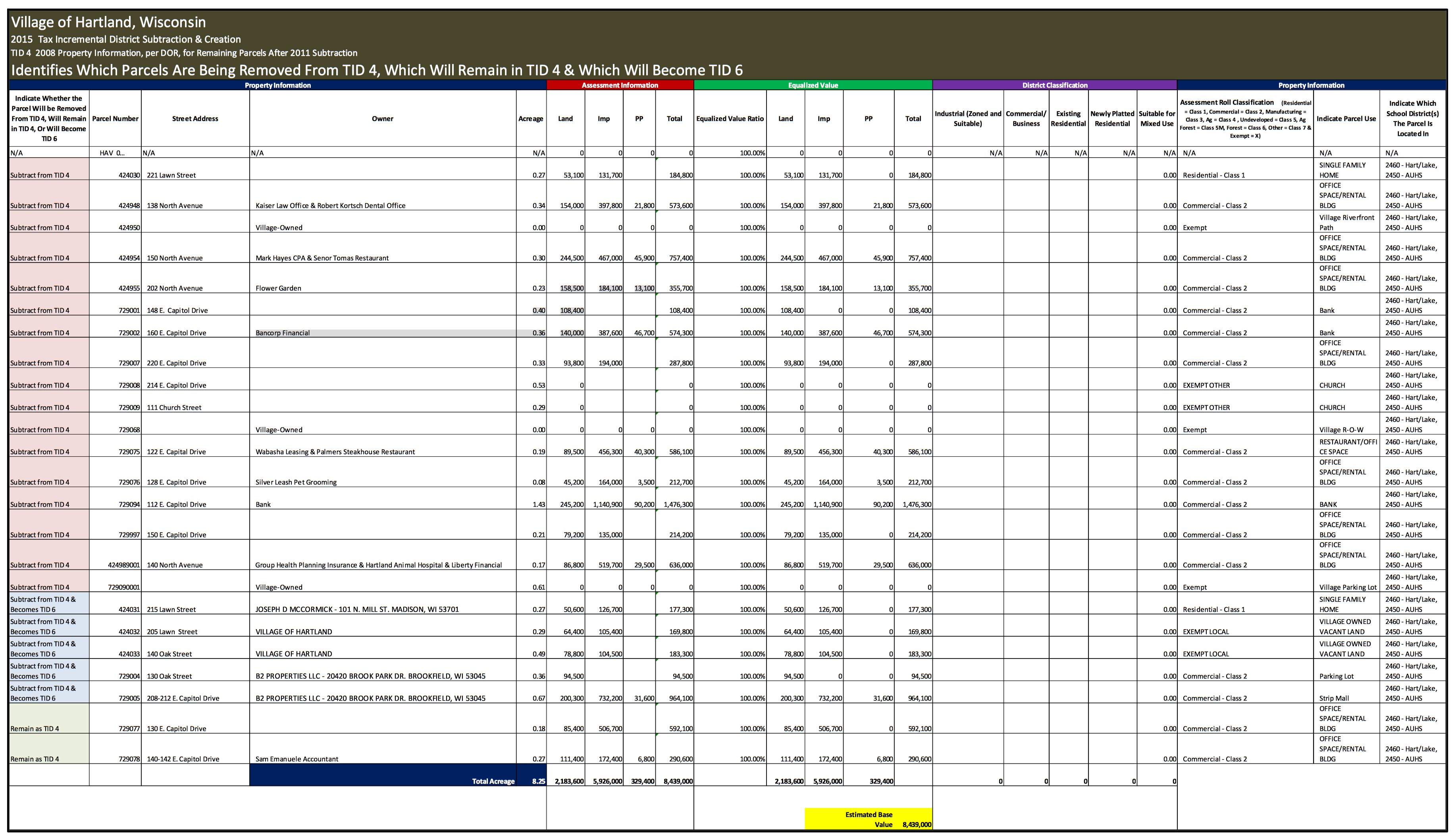

Neither Dave or Jim was willing to tell the public in straight forward, simple language, that the Village was giving two parcels that it had paid $415,487 for back in 2009 to McCormick as part of the TIF District 6 deal. They did not explain the arcane concepts of negative/positive increments or equalized values and they did not reveal that TIF District 4 had already recovered to a positive increment as of January 1, 2015. They did not provide any documentation supporting the notion that there would be a greater amount of tax increment if all the properties except two were removed. Did they consider only removing the 5 parcels they wanted to transfer to TIF District 6 and leaving all of the other parcels in TIF District 4; a course of action which probably would have recouped all of TIF District 4’s expenses given the overall recovery of equalized values in the district? (When The Buckthorn Man read this post, he chided me for being so naive. He explained that the Village didn’t care a whit if TIF District 4 recouped the costs attributed to it; there are no ramifications to the Village if TIF District 4 closes out with a deficit. The 17 properties removed from TIF District 4, and not transferred to TIF District 6, would all resume contributing a portion of their tax revenue to the 5 overlying taxing jurisdictions; they wouldn’t have to wait until TIF District 4 paid off it’s $649,220 deficit. That is why the Joint Review Board had no problem with the Amendment to TIF District 4. And the Village would also be able to resume using its share of tax revenue from the 17 parcels immediately without having to apply any of it to repay the TIF District 4 deficit). In case you are curious, here is a list of the parcels in TIF District 4, from the Project Plan, with the 5 properties destined for TIF District 6 highlighted toward the bottom, and the last two parcels being the only ones to remain in the amended TIF District 4 (click image to view full size).

President Lamerand asked for comments from the public and there were none.

Then they moved on to the TIF District 6 creation resolution, which, again you can listen to here. In a nutshell, they describe the $530,000 up front cash grant they are going to give to McCormick and the $1.2 million they are going to provide McCormick for the purchase of the two remaining properties in the new district (HAV 0729004 and HAV 0729005). They explain that this is being done so that McCormick could get an “acceptable” rate of return. And what is that rate? They don’t tell “the public”, and no one asks at the Public Hearing, but we found out from the Joint Review Board that it is 13%.

So, when describing the package being offered to McCormick to proceed with the Riverwalk development, Dave and Jim presented the scary and dubious proposition that TIF District 4 was in a “negative increment”, that removing most of the properties and transferring others to the new TIF District 6 would fix this (if it ain’t broke…), and they left unsaid the important information that there was a cost to the Village of $415,487 it used to buy the two parcels being donated. There were no questions or comments from the public.

Village Board Meeting and Public Hearing on June 22, 2015

The next step to making the amendment to TIF District 4 and the creation of TIF District 6 a reality was getting the Village Board to sign off; this was accomplished at the Board Meeting on June 22, 2015. Per the memo Administrator Cox included with the agenda packet regarding TIF District 4:

The District, which is currently in a negative position, will immediately move to a positive increment and is expected to generate tax increment sufficient to cover the loans made through the District and much of the funds expended by the Village in the District’s creation and implementation.

Again, we hear about the “negative position”, an assertion which the DOR data shown above demonstrates was factually inaccurate. Administrator Cox says that TIF District 4 is going to recover “the loans made through the District and much of the funds expended by the Village…”; a surprising statement given that Jim Mann had indicated at the Public Hearing on June 4 that the district was unlikely to “recoup” its expenses. And the deficit at the closure of TIF District 4 had grown even worse since then, to $355,213, as shown on the 6/22/2015 version of the Cash Flow table (shown above) presented to the Board. Nevertheless, given the positive trend in TIF District 4 value increments we saw in the DOR data above, I think the Village would have had the best chance of recouping their expenses if they would have amended TIF District 4 to only transfer out the 5 parcels they wanted to include in TIF District 6, and if they would have transferred the $415,487 cost used to buy the two parcels that were given to McCormick from TIF District 4 to TIF District 6 — where it belonged (see the comment from The Buckthorn Man above regarding the Village’s desire to “fix” TIF District 4).

Administrator Cox goes on to say that McCormick needs a little help if he is going to get the 13% return he needs to secure financing:

The Developer indicated that certain extraordinary costs associated with the project and other factors cause the project not to be economically feasible on its own. After review of the Developer’s costs and expected revenue, it was determined that public support in the form of grants would be appropriate to cause the development and allow the Developer to mitigate some of his risk and to anticipate an acceptable return. Under the terms of the Agreement, the $12 million development will be supported with $1.75 million in TIF funding comprised of $528,000 in grants to cover the immediate cost of utility relocation and installation and related engineering, building demolition, construction of a pedestrian bridge over the Bark River plus an additional $1.22 million to be paid by the Village over time from tax increment proceeds. The agreement would only be executed if TIF District 6 is finally approved and created.

Again, Administrator Cox fails to mention the gift of the two Village parcels, which it purchased at a cost of $415,487 back in 2009, as being part of the deal, or the fact that an additional $143,000 was being expensed to TIF District 4 with the conveyance of these parcels to the developer (see the 6/22/2015 version of TIF District 4 Costs above). The meeting agenda packet did include the PLANNED UNIT DEVELOPMENT AND TAX INCREMENTAL DISTRICT AGREEMENT, which explained that the two Village properties would be “conveyed” to McCormick, but nobody brought it up. Nor did Administrator Cox provide any documentation to support the “determination” that public support is “appropriate” and should be provided so that McCormick can get the 13% rate of return he needs.

Both resolutions were passed by the Village Board and there were no questions or comments during the Public Hearing.

Final Approval: Joint Review Board Meeting June 23, 2015

To effect the perfect “getaway”, Village Board President Lamerand, Administrator Cox and Mr. Mann needed to get the Joint Review Board to not only approve the Amendment to TIF District 4 and the Creation of TIF District 6, but also to disband and close out their participation in reviewing both of the TIF Districts. They had just voted to create TIF District 6 a few minutes earlier — what could possibly go wrong?

You can listen to the meeting here, it’s only 8 minutes long; that’s all the time it took to approve the amendment to TIF District 4, the creation of TIF District 6 and the disbanding of the JRB in regards to both TIF Districts. So much for due diligence. After all of their “work” was done and they began to discuss disbanding the Joint Review Board for TIF District 6, Mr. Mann described some pending legislation that would establish standing joint review boards and affect the way TIF Districts are reviewed and audited. Let’s take a look and see some of what the Legislature did. Paragraph (a) immediately below is the new language that will become effective on 10-1-16. The old language is included below that.

(4m) Joint review board.(a) Any city that seeks to create a tax incremental district, amend a project plan, have a district’s tax incremental base redetermined under sub. (5) (h), or incur project costs as described in sub. (2) (f) 1. n. for an area that is outside of a district’s boundaries, shall convene a standing joint review board under this paragraph to review the proposal. If a city creates more than one tax incremental district consisting of different overlying taxing jurisdictions, it shall create a separate joint review board for each combination of overlying jurisdictions. The joint review board shall remain in existence for the entire time that any tax incremental district exists in the city with the same overlying taxing jurisdictions as the overlying taxing jurisdictions represented on the standing joint review board.… (text here common to both versions)By majority vote, the board may disband following the termination under sub. (7) of all existing tax incremental districts in the city with the same overlying taxing jurisdictions as the overlying taxing jurisdictions represented on the joint review board.NOTE: Par. (a) is shown as amended eff. 10-1-16 by 2015 Wis. Act 257. Prior to 10-1-16 it reads:(a) Any city that seeks to create a tax incremental district, amend a project plan, have a district’s tax incremental base redetermined under sub. (5) (h), or incur project costs as described in sub. (2) (f) 1. n. for an area that is outside of a district’s boundaries, shall convene a temporary joint review board under this paragraph, or a standing joint review board under sub. (3) (g), to review the proposal.… (text here common to both versions)By majority vote, the board may disband following approval or rejection of the proposal, unless the board is a standing board that is created by the city under sub. (3) (g).

Mr. Cummings responded to Mr. Mann’s summation of the pending changes:

Mr. Cummings: You know I think it’s less than a band-aid. I mean, my big problem with TIF is there’s nobody, there’s nobody enforcing, enforcement. There’s stuff going on all over the place and nobody’s enforcing it (my emphasis). The only way we can enforce it is a lawsuit and obviously that’s not something that anyone would take lightly in doing that, ahhh, I guess it’s better than nothing.

But when I get, I get your reports, I review them. If I have questions, I call, and I’ve always have gotten responses to my questions. What’s not working, I think as it was intended back in — when the major revisions were made in the early 80’s — was the audit, that was being done. I think they thought there would be more things brought to the attention, like if you went over the project costs. I’ve never heard of an auditor comment that they went over the project costs or anything like that. Ummm, that’s not happening. And I don’t think audit firms want to take on that liability. I’m not sure that they foresaw that.

So unless you, you violate the department of revenue’s whole parcels, or you have more than whatever the percentage is of the Village etc…. The State does nothing. So it really is almost up to us that are regularly on these things to sort of birddog it (my emphasis).

Administrator Cox: So where does that cause you to land, pardon me?

Mr. Cummings: As far as this?

Administrator Cox: Yeah.

Mr. Cummings: We might as well disband (he says two more words that are unintelligible).”

Then Mr. Cummings moved to disband, President Lamerand seconded — all in favor? AYE!

Conclusion

The Village is currently building 3 new subdivisions with 2 more in the planning phases, none of which could be considered low income housing. In an attempt to create some “lower” income (rents start at only $1,000), high density housing, the Village made a generous explicit offer to JD McCormick, LLC for the Hartland Riverwalk Apartments development of $1.75 million. Behind the scenes however, hidden from view, occulted, the Village sweetened the deal by giving McCormick two parcels of land, for which it paid $415,487 of the taxpayer’s money — without telling them about this at the Public Hearings — and burying that cost in a TIF District that would never recoup the expense. Recall Mr. Cummings’ comment regarding the Village’s land gift to the developer at the May 27, 2015 JRB meeting transcribed above: “I wouldn’t have known that if you just didn’t tell me that”.

The shell game involved expensing $415,487 to TIF District 4 — which will never recoup the funds from incremental tax revenue — not TIF District 6, the obvious beneficiary of the land acquisition. And now, fully a year after the triggering events, the Village has recognized its obligation under the law to produce an audit of TIF District 4. Will that audit look only at the numbers in the books, or, will it also examine the way the deal went down? Would the birddogs on the disbanded Joint Review Board be interested in reviewing the audit?

I am done with the Village of Hartland Board, Adminstrator and DPW. It is clear from their actions that growing the tax base for the Corporation of Hartland is their all consuming goal. They don’t care about the Village of Hartland’s land at all, except its potential for development. In my dealings with the Village leadership I have encountered a stubborn refusal on their part to accept responsibility for maintaining all Village land or even to subject themselves to their own ordinances, which they enforce on everyone else in the Village.

I will continue my volunteer work at the Hartland Marsh on the Waukesha County Land Conservancy and Ice Age Trail Alliance properties.

CODA:

I attended the Village of Hartland Board meeting on July 11, 2016 to explain why I was resigning from the Environmental Corridor and Open Spaces Task Force. Have a listen.